What Is a Strata Insurance Valuation and Why Does Your Building Need One?

If you manage or own a lot in a strata scheme, you have probably seen the term strata insurance valuation on an agenda or in a levy notice without a clear explanation of what it actually means. Most people assume the insurer handles it. Some assume it is the same as the market value of the building. Both assumptions lead to the same outcome: a sum insured figure that is either too low to cover a real claim or too high and costing the scheme unnecessary premium dollars every year.

This guide explains what a strata insurance valuation is, what it measures, who prepares it, and why getting it right matters far more than most owners corporations realise until something goes wrong.

What a Strata Insurance Valuation Actually Measures

A strata insurance valuation is an independent assessment of the cost to demolish a strata building and rebuild it from the ground up to its current standard. It has nothing to do with what the building would sell for on the open market. The two figures serve completely different purposes and will almost never be the same.

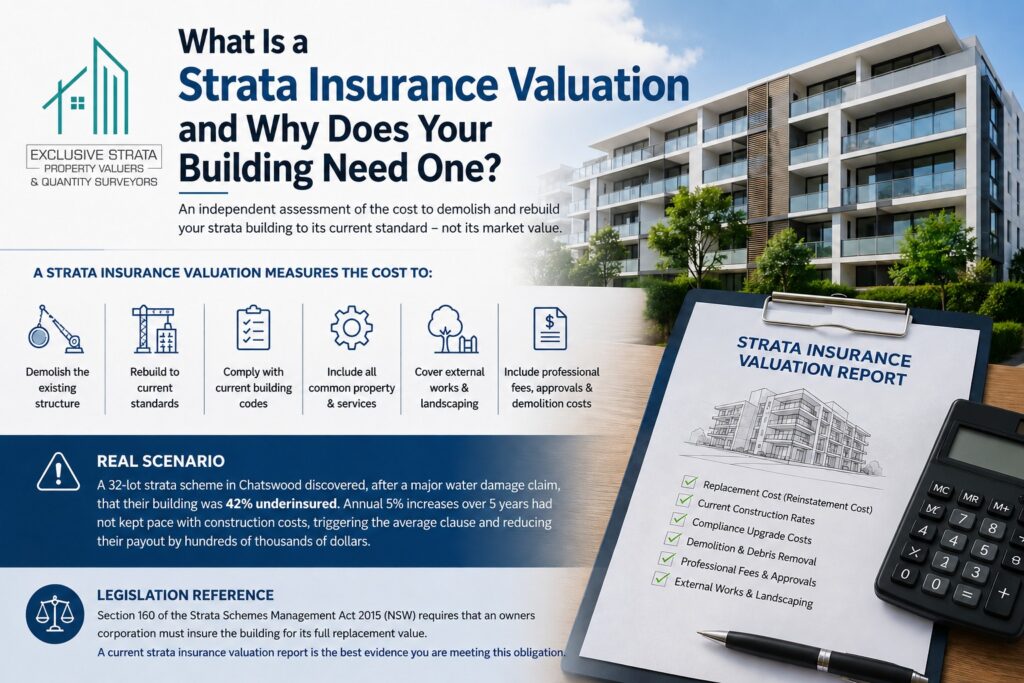

The technical term for what a strata insurance valuation calculates is the replacement cost or reinstatement cost. It includes the full cost of demolishing the existing structure, removing debris from the site, rebuilding the building to its current specification using current materials and labour, and meeting all current building code requirements that would apply to a new building on the same site today.

That last point is important. Building codes change over time. A building constructed in 2001 may not meet the fire safety, accessibility, or structural standards required under the National Construction Code today. If the building were destroyed and had to be rebuilt, it would need to comply with current standards regardless of what the original specifications were. A strata insurance valuation that does not account for the compliance upgrade cost will understate the true replacement figure.

What Is Included in a Strata Insurance Valuation Report

A properly prepared strata insurance valuation report is a detailed document. It does not simply provide a single dollar figure. It sets out the methodology used to calculate the replacement cost, identifies all components of the building that have been included in the assessment, and documents the cost assumptions applied.

The report will typically cover the structural shell of the building including foundations, floors, walls, and roof. It will include all common property fixtures and fittings such as lifts, lobby finishes, corridors, car park surfaces, and common area services. External works including driveways, landscaping, fencing, and retaining walls form part of the assessment. Professional fees for architects, engineers, and certifiers needed to obtain development approval and building permits are also included, as are demolition and debris removal costs.

A strata insurance valuation report for a well-managed owners corporation should be signed by a qualified professional and clearly state the effective date of the valuation, because replacement costs move with the construction market and a report that is three years old may be significantly understating current costs.

| Real Scenario |

| A 32-lot residential strata scheme in Chatswood had maintained its building insurance based on a valuation completed in 2019. The strata committee had increased the sum insured by five per cent each year at renewal on the advice of the broker, assuming this was sufficient to keep pace with inflation. In 2024 the building suffered major water damage from a burst pipe in the roof plant room. The insurer’s assessor determined the cost to rectify the affected areas was 1.9 million dollars. When the insurer reviewed the policy, it identified that the building’s actual replacement cost based on current construction rates was substantially higher than the sum insured. The average clause in the policy was triggered and the payout was reduced proportionally. The strata committee commissioned an independent strata insurance valuation immediately after settlement. The updated report showed the replacement cost was 42 per cent higher than the figure the building had been insured for. Annual premium adjustments of five per cent had not come close to keeping pace with actual construction cost movements over that period. |

Why Strata Buildings Are Frequently Underinsured

Underinsurance in strata schemes is more common than most owners corporations realise, and it happens for predictable reasons. The most frequent cause is that the sum insured has not been reviewed by an independent professional for a number of years. Broker-provided estimates, insurer calculators, and simple annual percentage increases applied at renewal are not substitutes for a proper strata insurance valuation report.

A second cause is that the original valuation used as the basis for the sum insured was itself inadequate. Developer-provided insurance valuations completed at the time of registration are often conservative and may not account for the full cost of compliance upgrades, professional fees, or the actual quality of finishes in the building.

The third cause is construction cost movement. The Australian construction industry experienced significant cost escalation between 2021 and 2024. Buildings that were adequately insured in 2020 may be materially underinsured today simply because labour and materials prices have shifted substantially. A strata insurance valuation that was accurate three years ago may now understate the true replacement cost by a wide margin.

| Legislation Reference |

| Section 160 of the Strata Schemes Management Act 2015 (NSW) requires that an owners corporation must insure the building for its full replacement value. The Act does not specify how replacement value is to be determined. This means the obligation to establish an accurate figure rests entirely with the owners corporation. Using an outdated or inadequately prepared valuation does not shift that responsibility to the insurer. |

Who Should Prepare a Strata Insurance Valuation

A strata insurance valuation should be prepared by a qualified professional with the appropriate credentials and expertise in construction cost assessment. In Australia, this typically means a quantity surveyor who is a member of the Australian Institute of Quantity Surveyors, or a Certified Practising Valuer with specific experience in building reinstatement assessments.

The distinction matters because insurance replacement valuations require a different skill set from market valuations. A market valuer assesses what buyers will pay for a property in the current market. A quantity surveyor with insurance valuation experience calculates what it will cost to demolish and rebuild a specific building to a specific standard at current construction prices. These are separate disciplines, and the most reliable strata insurance valuation reports are prepared by professionals who specialise in building cost assessment rather than those who treat it as a secondary service.

Owners corporations should be cautious about relying on valuations provided by the insurer directly or generated through an online calculator. These tools use generalised assumptions that may not reflect the specific characteristics of the building, and they are not independent assessments.

How Often Should a Strata Insurance Valuation Be Reviewed

The general guidance from the Australian Property Institute and the Australian Institute of Quantity Surveyors is that a full strata insurance valuation should be completed every three years, with a review or desktop update in the intervening years. However, this is a general guideline and not an absolute rule.

Buildings that have undergone significant renovation or improvement work, changed their configuration through subdivision or amalgamation of lots, added facilities such as rooftop amenities or car stacking equipment, or been located in areas where construction costs have moved substantially may need a fresh strata insurance valuation more frequently than the standard cycle.

The cost of commissioning an independent strata insurance valuation report is a legitimate expense of the owners corporation and is modest relative to the value of the building it is protecting. It is also modest relative to the financial consequences of a co-insurance clause being triggered on a significant claim.

Conclusion

A strata insurance valuation is not an administrative formality. It is the foundation of the most significant financial protection an owners corporation carries on behalf of every lot owner in the building. When the sum insured is based on an independent, current, and properly prepared insurance valuation for strata properties, the owners corporation can be confident that a genuine loss event will be met by the policy. When it is not, the gap between expectation and reality tends to emerge at the worst possible time.

| Need a strata insurance valuation report for your building? Exclusive Strata Valuers provides independent, AIQS-accredited insurance replacement assessments for owners corporations across Australia. Request a quote at exclusivestratavaluers.com.au |

Frequently Asked Questions

Is a strata insurance valuation the same as a market valuation?

No. A market valuation assesses what the property would sell for in the open market. A strata insurance valuation assesses the cost to demolish the existing building and rebuild it to its current standard using current construction rates. The two figures are unrelated and should never be used interchangeably.

How is a strata insurance valuation different from a building and contents valuation?

A strata insurance valuation typically covers the building structure and common property only, which is what the owners corporation is responsible for insuring under strata legislation. Individual lot owners are separately responsible for insuring their own contents and any improvements they have made to the interior of their lot that go beyond the standard of the original finishes.

What happens if our building is underinsured?

Most strata insurance policies contain an average clause or co-insurance provision. If the building is insured for less than its true replacement cost, the insurer may reduce any claim payment proportionally. For example, if the building is insured for 70 per cent of its actual replacement cost, the insurer may pay only 70 per cent of any claim, including partial loss claims that do not involve the whole building.

Can the strata manager arrange the insurance valuation, or does it need to come through the owners corporation?

Either approach is possible. The instruction to commission a strata insurance valuation report should ideally come from the owners corporation or executive committee, as the owners corporation bears the legal obligation to insure adequately. In practice, many strata managers coordinate the process on behalf of the owners corporation, but the report should be addressed to and retained by the owners corporation.

Does a strata insurance valuation include the contents of individual lots?

No. A strata insurance valuation covers the building structure, common property, and shared services and facilities. The contents of individual lots, including furniture, personal property, and owner-installed fixtures and fittings that are not part of the original building, are the responsibility of individual lot owners to insure separately under their own contents policies.