Building Reinstatement Valuation Explained: What It Is and Why It Differs From Market Value

Building reinstatement valuation is a term that appears regularly in strata insurance discussions, yet it is frequently misunderstood by the very people who need to act on it. Owners corporations, strata managers, and building committees often treat reinstatement cost and market value as interchangeable concepts. They are not, and confusing the two has real financial consequences when a claim is made.

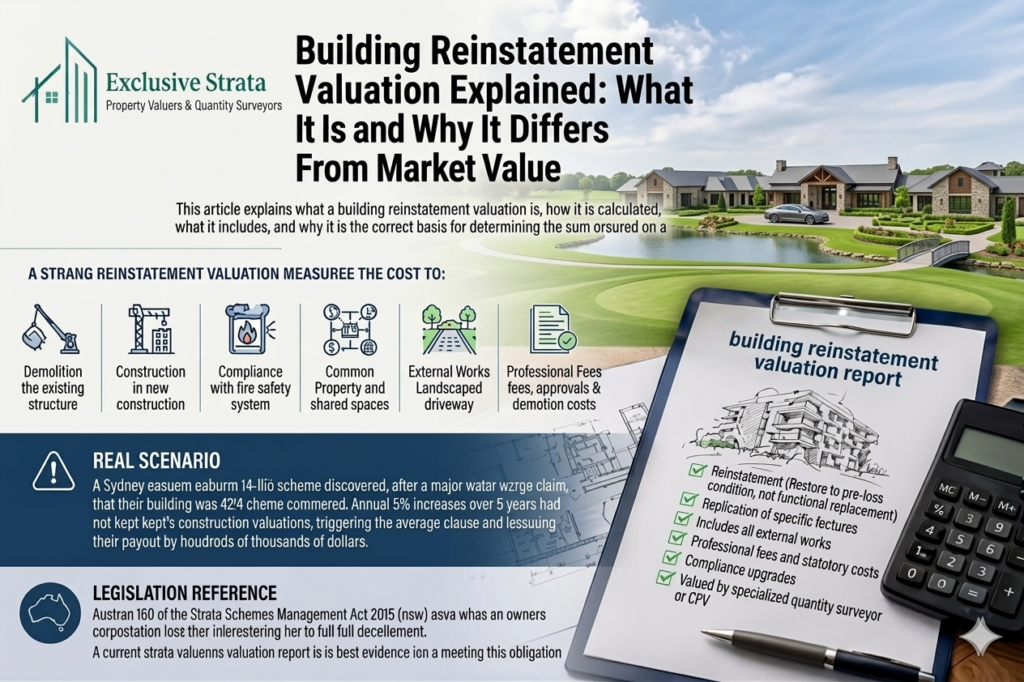

This article explains what a building reinstatement valuation is, how it is calculated, what it includes, and why it is the correct basis for determining the sum insured on a strata building insurance policy.

What Building Reinstatement Valuation Means

A building reinstatement valuation establishes the cost to restore a building to its pre-loss condition following damage or destruction. In the context of strata insurance, it specifically measures what it would cost to demolish the existing structure and rebuild it to its current standard, using current construction techniques, current materials, and current labour rates.

The word reinstatement is precise. It means restoring the building to what it was, not simply building something functional in its place. If the building had specific finishes, features, or construction methods, the reinstatement cost reflects what it would take to replicate those, not to substitute them with cheaper alternatives.

This is distinct from replacement cost valuation in some contexts, where replacement may refer to replacing a building with a modern equivalent that provides equivalent function but not necessarily equivalent specification. For strata insurance purposes, the terms reinstatement cost and replacement cost are generally used interchangeably, and both refer to the full cost of rebuilding the structure to its current standard.

How a Building Reinstatement Valuation Differs From Market Value

Market value is what a buyer would pay for the property in an arm’s length transaction in the current market. It reflects land value, location, demand, comparable sales, and the income potential of the property where relevant. It is the figure a real estate agent or property valuer would produce to guide a sale.

Building reinstatement value reflects none of those factors. It reflects only the physical cost of construction. A building in an area where land values are high will have a market value significantly above its reinstatement cost because the land component drives the price. A large industrial building in a regional area may have a reinstatement cost significantly above its market value because the physical structure is expensive to build but the land and location do not support a high sale price.

For strata insurance, market value is irrelevant. The insurer will pay what it costs to rebuild the physical structure. Using market value as the sum insured on a strata insurance policy will almost always result in either significant overinsurance or significant underinsurance depending on the relationship between land value and construction cost in the specific location.

| Real Scenario |

| A strata scheme of 14 lots occupied a building in Sydney’s eastern suburbs. The combined market value of the lots was approximately 28 million dollars, reflecting the premium location and strong buyer demand in the area. The executive committee had been using a sum insured of 25 million dollars, reasoning that this represented the building’s market value. When an independent building reinstatement valuation was commissioned prior to the policy renewal, the result was 8.4 million dollars. The building was a two-storey brick structure with no lift and standard finishes. The construction cost to rebuild it was a fraction of what buyers would pay to own it, because the land value was doing most of the work in the market value figure. The owners corporation had been paying premiums on a sum insured three times higher than it needed to be. The corrected reinstatement valuation allowed the committee to right-size the sum insured and reduce the annual insurance premium substantially. |

What a Building Reinstatement Valuation Includes

A thorough building reinstatement valuation covers all elements of the structure and common property that would need to be rebuilt or reinstated following a total loss. Understanding what is included helps owners corporations assess whether the valuation they have on file is comprehensive.

Demolition and Site Clearance

Before any rebuilding can occur, the damaged or destroyed structure must be demolished and the site cleared of all debris. These costs vary significantly depending on the construction type of the building, whether hazardous materials such as asbestos are present, and the accessibility of the site for demolition equipment. In dense urban environments, demolition and debris removal can represent a substantial portion of the total reinstatement cost.

Construction of the Building Structure

This is the core of the reinstatement cost and includes foundations, structural frame, external walls, roof structure, floor slabs, internal walls, windows, external doors, and all building services including plumbing, electrical, mechanical, and fire systems. The specification applied should reflect the current standard of the building, not a generic or average standard.

Common Property Finishes and Fittings

All common area finishes including lobby flooring, wall finishes, lift interiors, corridor carpets, and communal amenities form part of the reinstatement cost. Shared facilities such as pools, gymnasiums, rooftop terraces, and function rooms are included where they form part of the common property.

External Works

Driveways, car parks, pedestrian paths, landscaping, retaining walls, fencing, and external lighting all form part of the common property and must be included in the reinstatement cost. These elements are frequently omitted from inadequate valuation reports and their absence leads to systematic underinsurance.

Professional Fees and Statutory Costs

Rebuilding a strata building requires professional input from architects, structural engineers, fire engineers, mechanical engineers, and certifiers. Development applications must be lodged and approved. Building permits must be obtained. These professional fees and statutory costs typically represent between 10 and 15 per cent of the construction cost and must be included in a proper reinstatement cost valuation.

Compliance Upgrade Costs

A building that was constructed to a code that has since been updated may be required to meet current standards when it is rebuilt. This is particularly relevant for fire safety, accessibility under the Disability Discrimination Act, and energy efficiency requirements under the National Construction Code. A building reinstatement valuation that does not account for compliance upgrades will understate the true cost of reinstatement.

| Legislation Reference |

| Under Australian strata legislation across all states, the owners corporation bears the obligation to insure the building for its full replacement or reinstatement value. The Australian Property Institute’s guidance on insurance valuations states that the sum insured should reflect the cost of reinstatement as at the date of the insurance policy, prepared by a suitably qualified professional. A building reinstatement valuation that is more than three years old should be reviewed for currency. |

Who Should Prepare a Building Reinstatement Valuation

The appropriate professional to prepare a building reinstatement valuation for a strata building is a quantity surveyor with experience in building cost estimation, or a Certified Practising Valuer who specialises in insurance replacement assessments. Both disciplines have the skills to assess construction specifications, apply current cost rates, and produce a report that is defensible in an insurance dispute.

A reinstatement cost valuation prepared by a general property valuer without specific training in construction cost estimation, or generated by an online insurance calculator, is not a substitute for a properly prepared report. Insurers are aware of the difference and will scrutinise the basis of the sum insured more closely when a claim is significant.

Owners corporations and strata managers should retain a copy of the most recent building reinstatement valuation report as part of the scheme’s records. The report should be made available to lot owners on request and should be reviewed by the executive committee at each insurance renewal to determine whether a fresh valuation is needed.

The Relationship Between Building Reinstatement Valuation and Insurance Premium

The sum insured on a strata building insurance policy drives the insurance premium. A higher sum insured means a higher premium. This creates an incentive for owners corporations to keep the sum insured as low as possible, which can lead to underinsurance if the figure is reduced without proper justification.

Conversely, some owners corporations set the sum insured well above the actual reinstatement cost in the belief that this provides extra protection. This results in overinsurance and unnecessarily high premiums. An insurer will not pay more than the actual cost to reinstate the building regardless of how high the sum insured is.

The correct approach is to set the sum insured at a figure that reflects an independent, current building reinstatement valuation. This ensures the premium is appropriate for the actual risk and that the policy will respond fully in the event of a claim.

Conclusion

A building reinstatement valuation is a precise calculation of what it costs to rebuild a specific structure to its current standard at current prices. It is the correct basis for determining the sum insured on a strata building insurance policy and it is not the same as market value, an online estimate, or a figure carried forward from a previous year. Owners corporations that commission independent, current reinstatement cost valuations protect every lot owner from the financial consequences of underinsurance and ensure they are not overpaying premiums on an inflated sum insured.

| Need a building reinstatement valuation for your strata scheme? Exclusive Strata Valuers prepares independent, accredited insurance replacement valuations for owners corporations and body corporates across Australia. Request a quote at exclusivestratavaluers.com.au |

Frequently Asked Questions

What is the difference between a reinstatement valuation and a replacement valuation?

In the context of strata insurance, the terms are generally used interchangeably. Both refer to the cost of rebuilding the structure to its current standard following loss or damage. Some definitions draw a distinction where reinstatement means restoring to original specification and replacement means substituting a modern equivalent, but for practical insurance purposes in Australian strata schemes the two concepts produce the same figure.

Can we use last year’s building reinstatement valuation for this year’s renewal?

A valuation from twelve months ago may still be usable if construction costs in the relevant market have not moved significantly. However, given the level of cost movement in the Australian construction industry in recent years, it is advisable to have the report reviewed or updated annually rather than carrying the same figure forward without assessment. A qualified professional can advise whether a full revaluation or a desktop review is appropriate.

Is the land value included in a building reinstatement valuation?

No. Land value is not included in a building reinstatement valuation. The assessment covers only the cost of demolishing and rebuilding the structure. Land is not destroyed in a building loss event and does not need to be insured for replacement purposes.

Does a building reinstatement valuation cover individual lot interiors?

A standard building reinstatement valuation for a strata scheme covers the building structure, common property, and shared services and facilities. The internal finishes of individual lots are covered to the standard originally specified in the strata plan. Any improvements made by individual owners above that standard are the responsibility of those owners to insure separately.

How long is a building reinstatement valuation report valid for?

There is no fixed expiry period, but the Australian Property Institute and most insurers recommend that insurance valuations be reviewed every three years and updated as needed in the intervening periods. In a market where construction costs are moving rapidly, an annual desktop review is advisable to confirm the sum insured remains adequate.